My project It Makes Cents was created out of my frustration of the New Zealand schooling system. When I first left home I watched myself and my friends get thrown straight into the deep end of adult life without water wings or swimming lessons; and even though I felt like I was pretty responsible especially with money the amount of impulse spending and buying unnecessary things was wasting me a lot of money.

Every year there are young adults just like me transitioning from being financially dependent on their parents to becoming independent. The problem is that these young adults know little more than high school students do about personal money management but have a lot more freedom to make their own choices about money.

Research Methods

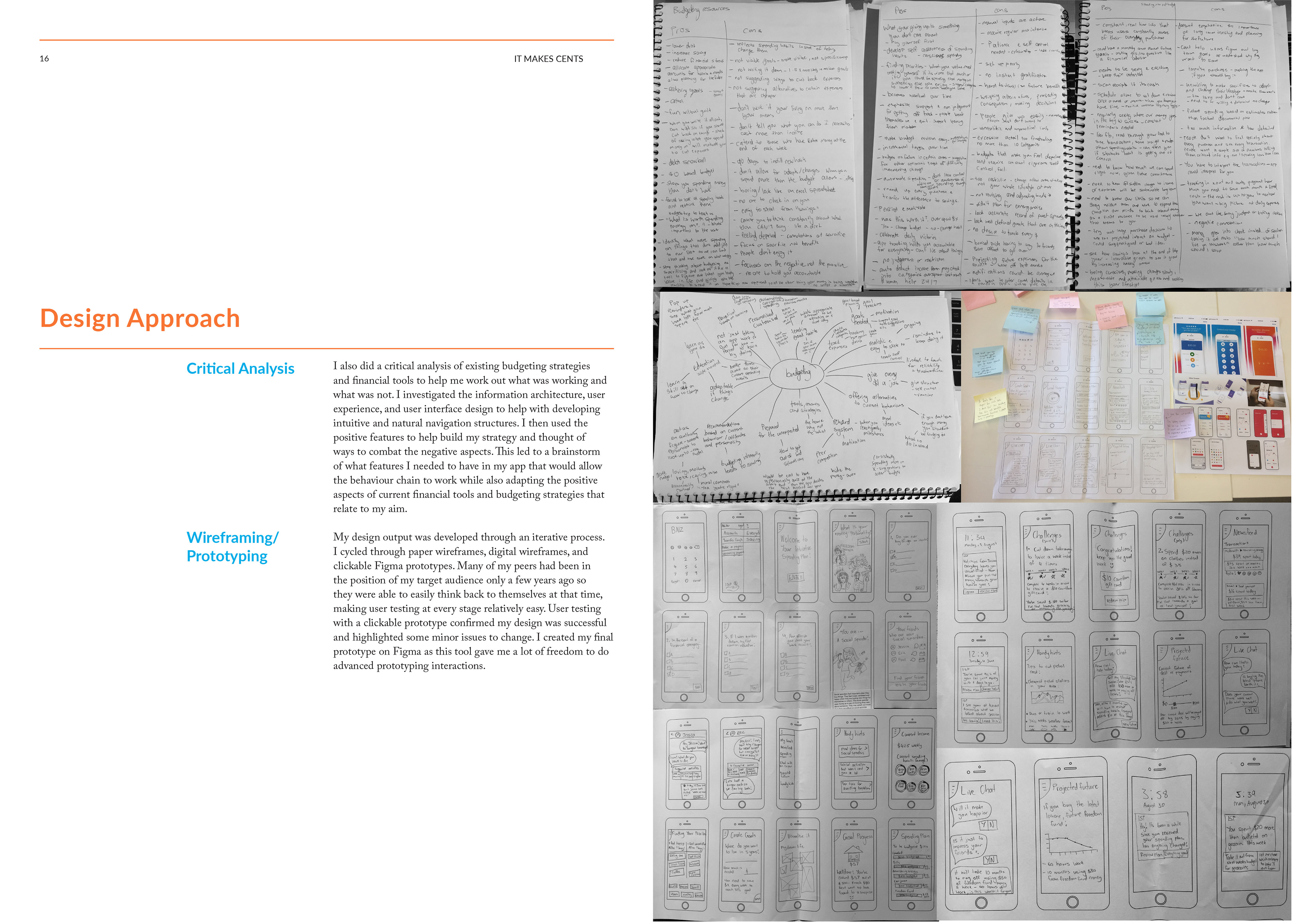

My process included a lot of in-depth academic and theoretical research on my topic. I critically analysed the strengths and weaknesses of existing financial tools as well as budgeting strategies. The Next Level Life financial YouTube channel was key in influencing my decision to focus on the benefits to the user and building wise financial habits through self-awareness and prioritising what you enjoy in life.

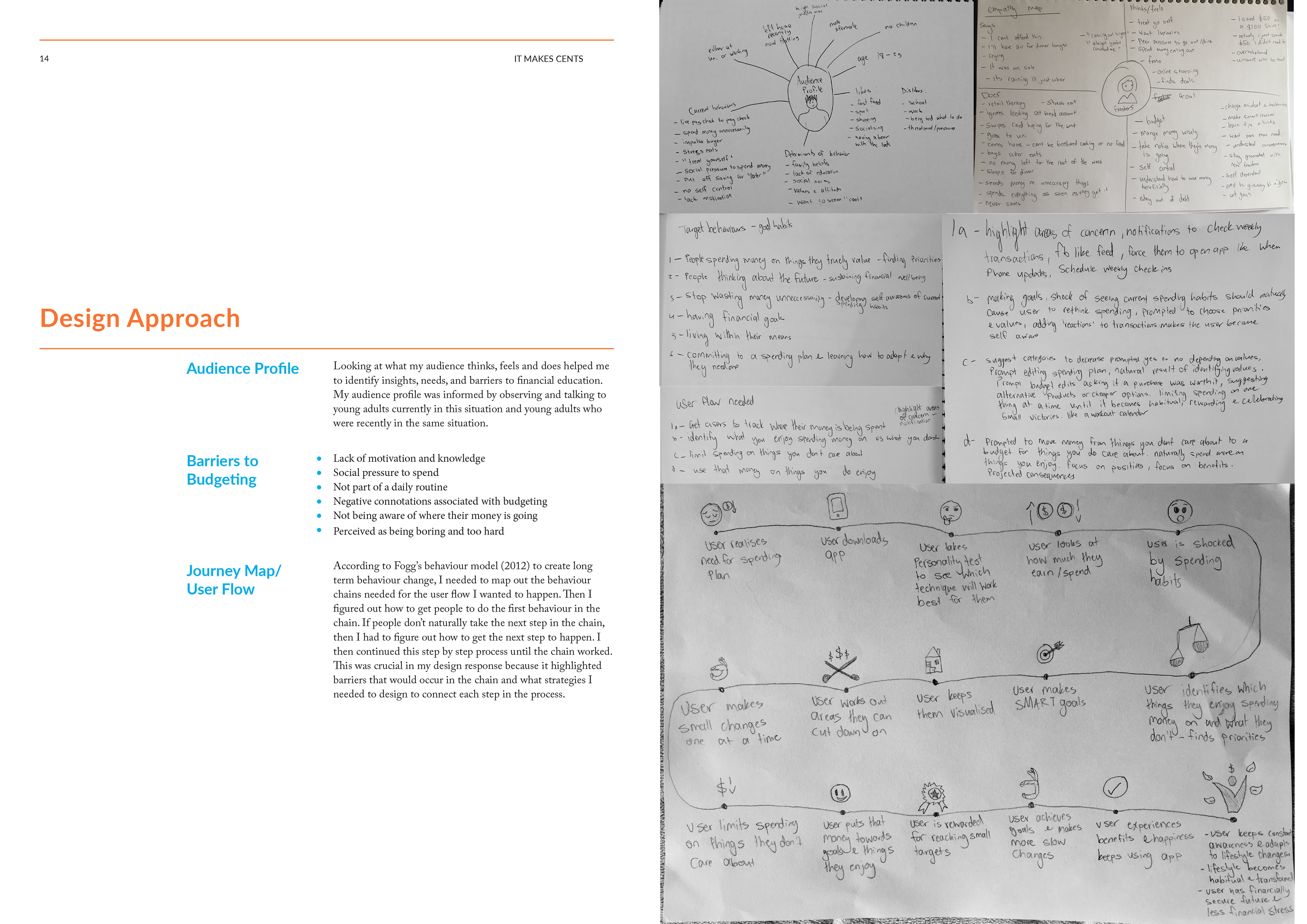

I paired theoretical and contextual research with human-centered research to find out how I could create a design solution that best suited the needs of my audience. I did this by conducting surveys, empathy mapping, interviews, journey mapping, and user testing. During this process the ethnographic research I conducted played a significant role in discovering motivations and what is required to inspire behaviour change in young adults’ financial habits. Casual interviews revealed that my audience needs a monetary goal in mind to motivate them to change behaviour. They also enjoy having conversations about money with peers and learning about their financial situations both to motivate, inspire and comfort them. They need easy and efficient solutions that only make small lifestyle changes to be effective. As a human-centered designer, I constantly tested my design response to these insights with my target audience to ensure it met their expectations and needs.

Instagram Ads

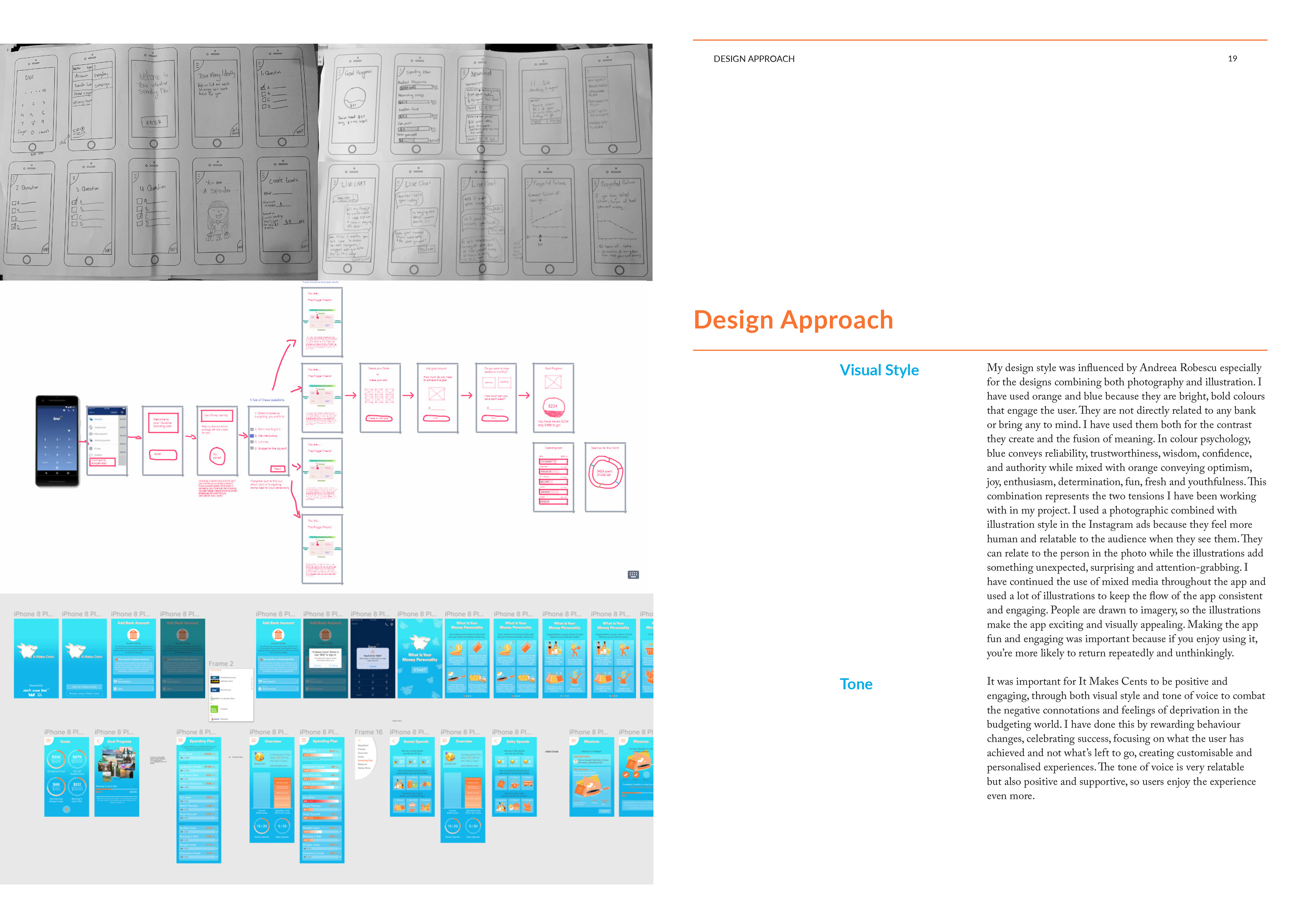

In the 4 stages of behaviour design, the first stage is to grab attention (Otani). I have created Instagram ads to draw people in with bright bold and attention-grabbing motion designs and stories. The Instagram ads are used to create interest and awareness of the app and get people excited and curious. The guilty confessions make it memorable, intriguing, relatable and humorous to the audience as they can see themselves in the confessions because “that’s so me”. By sending the message from people like them the brand comes across as friendly and approachable, not scary like normal financial apps. They are more likely to trust people like them and try the app out too. The ads also direct the user to the app store so they can download the app. The smart ads are customised by location and the person’s interests because people respond strongly to messages that are personalised and relevant to their behaviours, interests, and values.

Personality Quiz

The personality test keeps the fun attitude to start with and is used as a slow introduction into the serious stuff. It helps pace the app and connects it from Instagram ads to financial advice. By the time the user has found out their money personality, they are more likely to continue using the app because they are already invested and engaged with it. It asks questions about money using real-world relatable scenarios to the user.

Newsfeed

The newsfeed automatically downloads the user’s transactions, so they don’t have to manually input purchases and income as this is a hassle and too much work for my audience. The newsfeed follows the same experience as Tinder which will be natural and engaging to my audience. While the repetitive movements are addictive and enjoyable for the user, it is also forcing them to look at their spending habits and become self-aware of where their money is going. It takes the focus away from money and makes the user consciously think and reflect about what purchases they enjoy spending money on and the ones they don’t.

Goals

The goals are there to make sure the user is saving for a purpose and has something they want to work towards not just saving for the sake of it. The emergency saving goal is automatically set up for the user based on what the app thinks is an appropriate amount to save weekly constructed from their income and spending habits. When creating a goal, you have the option to have one suggested for you such as paying off debt. You can also get suggested $ amounts based on people like you and the average amount users spend on goals like this. The recommended weekly payment is based on how much you need to save to achieve the goal in the time frame and how much income you earn. The suggested time frame is also recommended based on how much you need to save and the amount that’s realistic for you to save weekly. If you do all your own inputs the app gives you a likelihood meter based on if it thinks this is a reasonable goal to achieve in the time frame you want.

The next step is to visualize the goal because keeping things visualized is motivating (Clear). When you can see it and you’re constantly reminded of where you could be soon, you’re less likely to use that money on something else because you are saving for a purpose that you enjoy and you don’t want to steal money from something that will make you happy.

The last stage in behaviour design is to sustain behaviour. Taking action once is not enough. For my app to have a long-lasting impact it needs to motivate people to continue their behaviour and feel a sense of progress over time (Otani). Therefore, I have made sure my design celebrates progress and rewards the user with positive feedback and incentives. When checking goal progress, the user is offered incremental rewards to keep them motivated to keep saving. They will feel like they’re successful and making positive progress by adding immediate value to the experience instead of having to wait the whole time frame. Instead of focusing on how far is left to go I am reinforcing the positive aspects by rewarding how much has been achieved so far.

Spending Plan

To combat the negative connotations of the word budgeting I have called it a spending plan where the focus is not on money it’s on goals and enjoyment. The spending plan utilises techniques from the value-based and zero-dollar budgeting techniques. I have chosen to use these strategies because it forces the user at least once to look at where their money is going and the knowledge of where it’s been going can be life changing for some people. It forces the user to live within their means because they are only allowed to allocate what they’ve earned to the categories. It’s hard to waste a dollar if every dollar has a purpose. Being in control of your money instead of it being control of you can be empowering.

The app automatically downloads income and expenses so that if the user overspends in a category, they can either take it out of a different category with leftover money in or the app automatically takes it off next week’s income. I have made the default option of the app automatically setting amounts for each category because people are lazy and can’t be bothered doing it themselves and if they want to do their own amounts, they can edit it. The recommended amounts are personalised based on the sweet and salty purchases the user identified in the newsfeed and their previous 6 months’ spending habits. It considers the goals the user wants to achieve does the math work to allocate a realistic weekly amount. The app allocates less to salty categories and more to sweet categories but only very small changes from current spending habits, so the users feel as though this is an achievable and realistic amount and don’t feel limited or deprived. If the user is currently spending more than they earn, the app may not allocate any money to goals because I want the user to gradually change habits slowly, over time. If the user is completing a mission, it will allocate less to the category it is targeting based on the predicted savings.

Missions

The missions are based on the user’s salty purchases. The app creates a personalised mission to help them change one spending habit at a time that is not bringing them joy. It is all well and good to identify what you don’t like spending money on but it’s hard to stop spending money on it when you don’t know how to stop. By making gradual, small changes over time it becomes natural and habitual. Being rewarded and focusing on positive reinforcements offers the user immediate value and motivates them to keep working towards the goal. Once a mission is completed, the user receives a reward in line with the category it was targeting. The next challenge will be a different category the user feels salty about. Making small alterations to bad habits over time but not cutting things out completely will leave the user feeling empowered and not like a failure because they are more likely to stick to it if it feels easy. Making people feel successful triggers a positive emotional response associated with the app and makes them more likely to return (Fogg). Being rewarded as well as seeing money being saved from altering a habit in a small way helps the user develop a stronger motivation for the new behaviour so that the old habit is relatively less motivating (“How to Design for Long-Term Behavior Change”). They recognise the value of participating in the missions which drives them to keep returning and reaching the target mission as well as being a fairly easy change because nothing is being cut out completely. There are no feelings of deprivation or sacrifice. Small changes over time and one at a time is key to habit changing (Fogg).

Friends

Friends are added by searching their name or by contact. It gives the user a sense of community by seeing their friend’s money personalities. Developing a community combats the isolation people sometimes feel when going against social norms. They can chat via the app and if they are having trouble trying to organize an event that won’t cost them too much, the app offers suggestions for their personality type. Both people click on the option they want and if it’s the same an event is created, if not they can work it between themselves. The goal is to give the user some creative solutions and ideas to solve their problems.

Overview

The overview shows the user how much money they have right now as sometimes we’re out shopping and need to know the exact amount we have in our account instead of having to work out the maths. It also shows the user where their money has been spent this week visually. There is an overview of the user’s sweet and salty spends, how many purchases are going to each and what their top 3 of each are. It also lets you see your friend’s top 3 sweet and salty spends. This gives a sense of community and support and lets the user know they are not alone.

Handy Hints

Handy hints are a similar feature to the chat; however, they are more generalised, and the user can go through and find activities for their personality type that won’t cost a lot but will still meet their social needs.

There is also personalised advice. The app provides cheaper alternatives to current plans the user may be on whether that’s phone or internet company’s or insurance to find them the best deal that’s right for them.

Conclusion

At the beginning of the year, I had the goal of improving financial literacy in general for all children leaving school, but I realised this is a huge task and won’t be able to be solved with one tool or resource. I had to change my focus to making one small contribution towards someone’s financial wellbeing. I got very absorbed in the research side of things looking at models of transformative behaviour, motivation theory and personality theory and how both internal and external factors affect someone’s financial decision making. All of which are important and were considered in my final design output, however, as a designer it was important to narrow down my scope to focus on one goal so that I could achieve this within the time frame, using my skills and expertise.

I acknowledge that I am not an expert in psychology and I would have liked to work more alongside professionals in this field as well as financial advisors. Working with these two professions is a future opportunity to develop It Makes Cents further. If It Makes Cents were to exist in the real world, I would like to have more touchpoints. I chose an app due to accessibility, customisability and personalised features, however, having a website version, as well as a physical print-based option, would cater to those who enjoy having tangible experiences and would appeal to a wider audience. I would also like to have more campaigns that show its adaptability to different incomes and lifestyles. A YouTube channel explaining the research side of things such as positive and negative aspects of budgeting strategies, the thought process behind the app strategy as well as verbally and visually showing the handy hints and different ways to use the app would be beneficial to the experience.

I believe It Makes Cents would be successful in the real world. It offers a unique addition to the financial education environment because it addresses the psychological aspects of behaviour change and focuses on practical skills rather than simply imparting knowledge. It also offers an alternative perspective on money that no other resource utilises so that the user views money as a tool rather than an enemy. It focuses on the user’s joys in life and how

to achieve them, providing a unique benefit to the user that doesn’t result in the feeling of sacrifice. It’s enjoyable and motivating to use which will facilitate returning users. It has the potential to make a long-term positive impact on financial wellbeing.

to achieve them, providing a unique benefit to the user that doesn’t result in the feeling of sacrifice. It’s enjoyable and motivating to use which will facilitate returning users. It has the potential to make a long-term positive impact on financial wellbeing.

For more information about my design process take a look at my workbook blog: https://hannahvcdresearchproject.blogspot.com/